Introduction – why “permanent life insurance” deserves a second look

When people hear permanent life insurance they often picture an expensive policy that financial salespeople push on retirees. That’s a half-truth. Permanent life insurance does cost more than term coverage, but it also combines a death benefit with a cash-value component you can use while you’re alive – and that blend can solve real planning problems when used intentionally. In this guide I’ll walk through what permanent policies actually do, the different flavors (whole, universal, indexed, variable), the real benefits and the real pitfalls, and-most importantly-when this kind of policy makes sense. Investopedia

Quick primer: what permanent life insurance is (and what it isn’t)

At its core, permanent life insurance provides coverage for your entire life (so long as premiums are paid) and usually includes a cash-value account that grows tax-deferred inside the policy. That cash value can be accessed via loans or withdrawals, or left to grow and increase the death benefit. Think of it as life insurance + a savings/investment wrapper. Investopedia+1

Key point: The death benefit is generally paid to beneficiaries income-tax free (with some exceptions), which is a major reason people use life insurance for estate planning. The IRS confirms that life insurance proceeds received because of an insured’s death are usually not taxable income. IRS

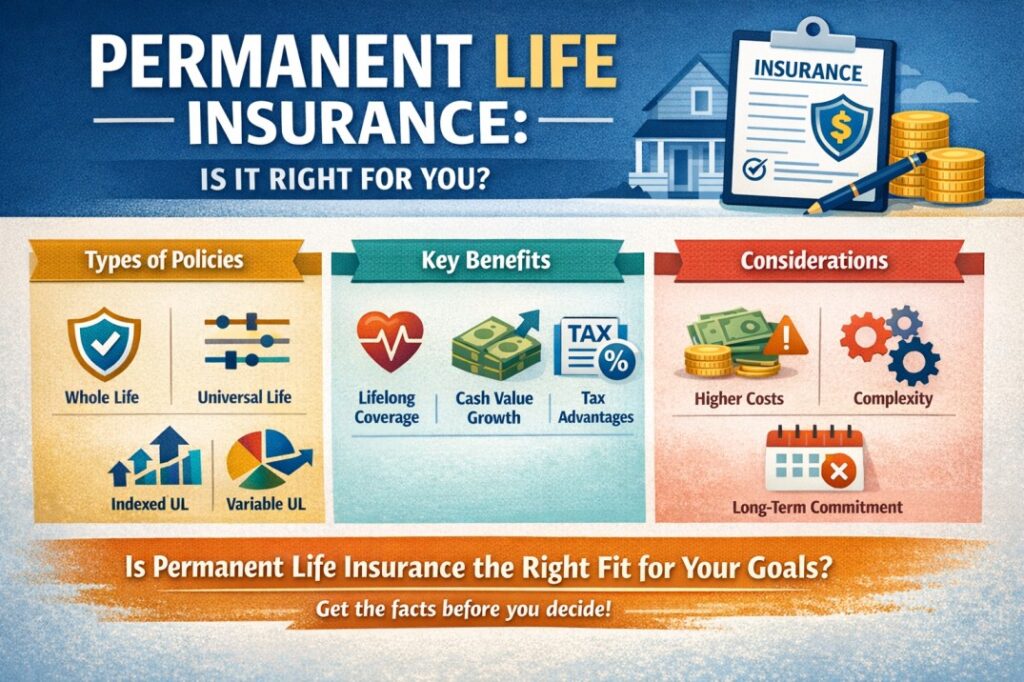

Types of permanent life insurance

- Whole life: Fixed premiums, guaranteed cash-value growth, predictable performance and dividends for some mutual insurers. Good for conservative, long-term planning. Investopedia

- Universal life (UL): Flexible premiums and death benefit. Cash value earns interest tied to the insurer’s declared rate; more flexibility but more moving parts. NerdWallet

- Indexed universal life (IUL): Cash-value growth is linked to a market index (e.g., S&P 500) with caps and floors—potential upside but with complexity and cap mechanics. Suitable for those who want market-linked growth without direct stock exposure. Forbes

- Variable universal life (VUL): Cash value invested in subaccounts like mutual funds — highest upside and downside risk; treated like securities. Investopedia

At-a-glance comparison

| Feature | Whole Life | Universal Life | Indexed UL (IUL) | Variable UL (VUL) |

|---|---|---|---|---|

| Premium predictability | High | Flexible | Flexible | Flexible |

| Cash-value growth | Guaranteed (modest) | Interest-based | Index-linked (cap/floor) | Market returns (high variance) |

| Complexity | Low | Medium | High | High |

| Risk to cash value | Low | Medium | Medium (caps/participation) | High |

| Typical buyer | Conservative, estate planners | People wanting flexibility | Those wanting upside w/ downside protection | Investment-savvy buyers |

Real advantages people actually use

- Tax-efficient accumulation and access. Cash value grows tax-deferred; policy loans are generally tax-free if structured properly. This can be useful once retirement accounts are topped out or for creating a supplemental, tax-efficient source of liquidity. (Be careful-loans reduce the death benefit if unpaid.) Investopedia+1

- Guaranteed lifelong coverage. For people with ongoing obligations (e.g., special-needs children, estate liquidity needs) permanent coverage removes the risk of outliving a term policy. Investopedia

- Estate and legacy planning tools. High-net-worth individuals use permanent policies (often held in trusts) to provide tax-efficient inheritances or to fund estate taxes and business succession plans. Investopedia

- Policy flexibility and riders. Many permanent policies offer riders-accelerated death benefits, long-term care riders, guaranteed insurability-that can match evolving needs. Investopedia

The trade-offs (what makes critics nervous)

- Cost: Premiums are significantly higher than term life for the same death benefit. If your priority is pure income replacement at low cost, term + investing the difference may win. Many personal-finance experts caution against using IULs or VULs as primary retirement vehicles without careful modeling. NerdWallet+1

- Complexity and assumptions: Policies like IUL and VUL rely on caps, participation rates, credited rates, and fees. Poor projections or persistent low performance can erode cash value and require higher premiums later. Forbes+1

- Surrender charges & early years: Cash-value features are back-loaded; surrendering early often triggers large fees and losses. Permanent insurance is generally a long-term commitment. Investopedia

When permanent life insurance makes sense

- You need lifelong coverage (for dependents with lifetime care needs).

- You want an estate-planning tool to provide liquidity for taxes or inheritances and you’ve already maxed out retirement vehicles.

- You want policy loans as a planned source of tax-efficient liquidity in retirement, and you accept the longer horizon and costs.

- You run a business and need buy-sell funding or key-person protection that lasts past core employment years.

If none of these apply, term life plus investing the premium difference is often the simpler, lower-cost choice. NerdWallet and other consumer resources commonly recommend term for most wage-earners and permanent only for specific planning reasons. NerdWallet+1

How to evaluate offers – a five-step checklist

- Run a cash-accumulation comparison (cash accumulation method) that compares expected cash value vs. alternatives. Don’t accept a single projected rate without understanding assumptions. Investopedia

- Ask for an Illustrated History of the policy’s projected cash value under conservative, moderate, and optimistic scenarios (and get them in writing).

- Check fees and cost structure: mortality charges, admin fees, surrender schedule, and rider costs.

- Understand loan mechanics: interest rate, how loans affect the death benefit, and consequences of unpaid loans.

- Stress-test for a market downturn (for IUL/VUL): what happens to premiums and cash value if growth stalls for 5–10 years?

Perspective

Three typical outcomes in real life: (A) a conservative whole-life policy held for decades that became a quiet, reliable legacy tool for a family; (B) someone who bought an IUL expecting 8–10% annual credited returns and later needed to inject cash when returns were lower; and (C) people who bought term and invested the difference and ended up with a larger nest egg but no permanent death-benefit safety net. There’s no one-size-fits-all answer-permanent insurance is a tool, not a one-stop solution. Use it when its unique attributes (lifelong coverage + liquidity + tax efficiency) match specific goals. Investopedia+1

Practical example

Imagine two 35-year-olds each want $500,000 of protection.

- Term (20-yr level) might cost $30/month (age and health dependent).

- Whole life for the same face could cost $300–$600/month but builds guaranteed cash value and may pay dividends.

This huge premium gap is why permanent policies are often targeted: if you need only income replacement for the next 20 years, term is the efficient choice; if you need lifelong coverage or cash-value features, permanent may be worth the cost.

(Always get real quotes — these are illustrative.) NerdWallet

Common mistakes to avoid

- Treating IUL/VUL as a simple investment account. Those policies have caps, participation rates, and fees that change the risk/return profile. White Coat Investor

- Skipping the stress tests. Ask for worst-case scenarios and understand what happens if you stop paying extra premiums.

- Buying without an estate plan. If your goal is legacy or tax efficiency, make sure the policy is structured with trusts or beneficiary designations to match your estate objectives. Investopedia

Final verdict

Permanent life insurance is neither a scam nor a magic bullet. It’s an expensive but powerful combination of lifelong protection and tax-efficient accumulation. For most people, term life plus disciplined investing will be the fastest, simplest route to financial security. But for specific needs-estate liquidity, guaranteed lifelong coverage, or a managed source of tax-efficient retirement liquidity-permanent life insurance can be the right tool when purchased with eyes wide open.

Disclaimer: The content provided is for educational and informational purposes only and should not be considered financial, investment, insurance, or legal advice.